How Embedded Payments Put Real Money Back in Your Store

If you run a dealership, you know how the end of the day usually goes.

The doors are closed, customers are gone, and someone is still at a desk trying to make reports, receipts, and bank totals agree. Card batches in one place, POS in another, spreadsheets somewhere in between. Nobody goes home until it all lines up.

Embedded payments are designed to fix that. Not by adding another system, but by connecting the ones you already use so the payment work mostly takes care of itself.

By connecting your payment processing directly with your POS and accounting systems, you turn a daily headache into a profit center, often recovering up to $17,500 a year that you can put back into growing your business.

Click to Jump Ahead:

1. The Hidden Cost of Manual Reconciliation

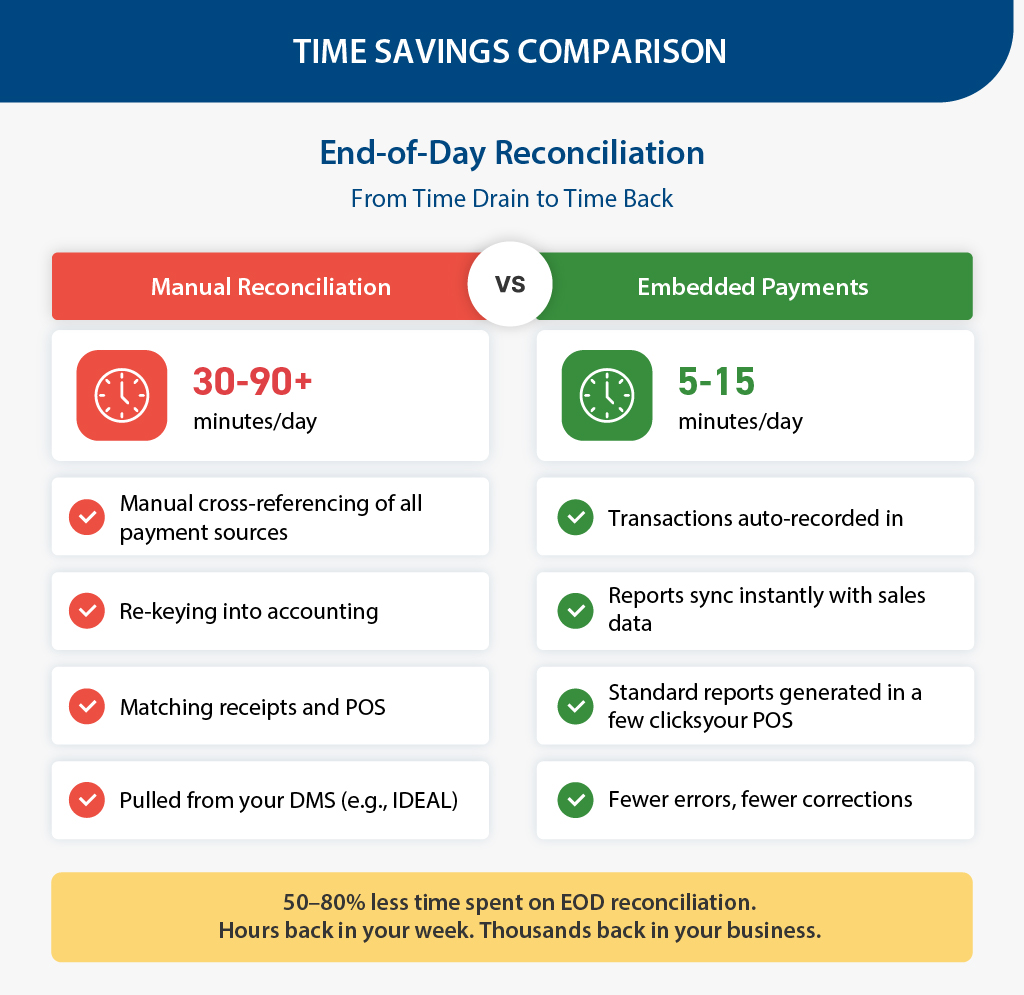

End-of-day (EOD) reconciliation is a perfect example of invisible waste.

Without embedded payments, most businesses spend 30–90+ minutes every day:

- Manually cross-referencing every payment source

- Re-keying totals into accounting software

- Matching receipts and POS reports by hand

- Running extra review cycles to chase down discrepancies

This is slow and error-prone. Every typo, mismatch, or missed transaction costs extra time to fix and increases the risk of chargebacks or inaccurate books.

With embedded payments, that same process drops to 5–15 minutes a day:

- Transactions are auto-recorded in your POS

- Payment reports sync instantly with sales data

- Standard reports are generated in a few clicks

- Fewer errors mean fewer corrections, period

Embedded systems routinely cut EOD accounting time by 50–80%. Over a year, that’s hours back in your week and thousands of dollars in regained productivity.

Read Next: How to Optimize Your Service Department Processes Using Technology

2. Key Features That Drive ROI

The financial impact is tied directly to how integrated payments work in your day-to-day operations.

Auto‑Sync Transactions

Every sale posts into your system right away. No double entry, no missed tickets, no “I’ll update it later.” Your books stay current without extra effort.

Unified Payment Reports

Credit, debit, mobile payments, and cash all show up in one place. Reconciliation that used to take close to an hour can often be wrapped up in a few minutes.

Error Detection and Alerts

The system flags mismatches for you. That means you catch problems quickly, instead of finding them days later when they are harder to fix or have already turned into disputes.

One‑Click Reporting

Daily, weekly, and monthly summaries are ready when you need them. You spend less time building spreadsheets, and you have cleaner reports to share with your accountant or management.

POS and Accounting Integration

Your payment solution connects directly to the tools you already use. That removes duplicate systems and cuts down on tedious re‑keying between platforms.

Chargeback Reduction

Clear, accurate transaction records reduce the number of disputes you see. That also cuts back on chargeback fees in the $15-$25 range that slowly chip away at your margins.

3. Putting Real Numbers to the ROI

To see what this looks like over a year, here’s an example.

Assume:

- Annual revenue of around $500,000

- One main person handling reconciliation at $20 per hour

- A current end‑of‑day process that takes close to an hour

With embedded payments, it is realistic to cut that end‑of‑day time by half or more.

Using 50 minutes per day saved as a working number:

- Labor savings

About $5,040 per year from time moved away from manual reconciliation into higher‑value work. - Lower bookkeeping costs

Cleaner, automated data can reduce outside bookkeeping by around half, worth roughly $2,250 per year for many small and mid‑sized operations. - Fewer chargebacks and fees

Better records and fewer errors reduce disputes. Avoiding just 5 disputes a month at about $20 each comes to $1,200 per year - Revenue lift from smoother checkout

Faster, more reliable payment experiences tend to increase completed sales. A modest (2%) bump of $500,000 in revenue is another $10,000 per year

Add those together, and you are looking at a realistic potential of more than $17,000 per year in savings and added revenue for a typical store.

Your exact numbers will differ, but the structure holds: less wasted time, fewer problems, and more capacity to sell and serve.

Read Next: Dealership Inventory Management Guide

4. How Dealers Put That Money to Work

Once that money is no longer tied up in manual work and avoidable fees, you can point it at areas that actually grow the business. For example:

- Inventory and parts ($4000-$6000)

Put a few extra thousand dollars into the brands, models, and accessories customers keep asking for. Better stock often means higher average tickets. - People and training ($2500-$4000)

Use a portion of the savings on sales and service training. Well‑trained staff close more deals, protect margins, and create repeat customers. - Technology upgrades ($2000-$4000)

Improve your POS, add online booking or payments, or tighten up the tools your team uses every day. Small improvements here can pay back quickly. - Marketing & customer acquisition ($3000-$5000)

These are the kinds of moves that are hard to make when every spare dollar is eaten up by inefficiency. Embedded payments help free up that budget.

Are Embedded Payments Worth It for Your Store?

You do not need a complex model to get a first look at your own ROI. Start with a few simple questions:

- How many minutes per day are you spending on reconciliation and fixing payment issues?

- What is the hourly rate of the people doing that work?

- How much are you paying each year for outside bookkeeping?

- How often are you dealing with chargebacks or disputes?

If you are spending too much time fixing payment reports at the end of the day, you are probably leaving money on the table.

Embedded payments can help you get that time and money back.

See how embedded payments could work in your dealership!